Predicting De-globalization - Peter Zeihan (Part II)

‘God has a special providence for fools, drunkards, and the United States of America.’

This is Part 2 of a two-part, high-level overview of Peter Zeihan’s views on geopolitics and de-globalization. These articles sit within a broader series covering analysts that have been predicting de-globalization for the past several years.

Part 1 covered Zeihan’s historical-political framework describing the formation of the post-War global Order, secured by American military strength, as a result of America’s efforts to win allies against the Soviets. This article will cover the geographic and demographic factors that allowed the U.S. to play the role of guarantor of the Order and will allow the U.S. to weather the dis-integration of that Order as it retreats from this role.

The boons of place

My understanding of Zeihan’s take on the strategic advantages reaped by America from its geography is fairly simple and straightforward. They can be divided into roughly two categories: oceans and energy. Both are relatively well-known advantages, but they interface with the historical-geopolitical framework laid out above in interesting ways.

The USA is a continent spanning country nestled between two massive oceans. Historically, oceans, deserts, mountain ranges, and other forms of hostile terrain formed natural borders between communities. These natural landscapes served as defensive boundaries, repelling attacks and allowing societies that were well positioned to grow with relatively little disturbance. As technology progressed, it eroded the effectiveness of these natural repellents, but they still form an important part of any country’s security strategy.

The U.S. has historically benefited from these massive oceans. They increased the cost of invading the country for its enemies, allowing people and infrastructure to develop relatively unperturbed. Miraculously, somehow, the U.S. has managed to avoid the strategic law laid out by the ancient Indian political theorist, Kautilya in his mandala siddhanta framework — one’s neighbor is one’s natural enemy.

The U.S. used to have serious clashes with its neighbors, but for generations now those relationships have been remarkably stable. I suspect a combination of relative U.S. power advantage, belief in the lack of U.S. desire for conquest, belief in the U.S.’ willingness to defend its neighbors from attack, and the prospective benefits of establishing economic linkages with the U.S. all play into Mexico and Canada maintaining cordial relationships with America. How exactly North America arrived at this historically anomalous situation is a subject worthy of in-depth study.

The second geographic advantage is energy. Thanks in large part to technologies like fracking, the U.S. became a net energy exporter a few years ago. According to Zeihan, this officially dissolves one of the few strategic interests that would have kept the U.S. actively engaged in maintaining the global trade system in the coming years — domestic fossil fuel demand. Here is an excerpt from the description of his 2017 book, The Absent Superpower:

The American shale revolution does more than sever the largest of the remaining ties that bind America’s fate to the wider world. It re-industrializes the United States, accelerates the global Order’s breakdown, and triggers a series of wide ranging military conflicts that will shape the next two decades.

The U.S. has abundant natural resources to satisfy its own needs, cordial relationships with its neighbors and two massive oceans to protect itself from enemies. Though it defended the inter-connected global trade regime, the U.S. itself never became heavily dependent on it for its own economic survival. Therefore, it can leave that system without existential threat to its own society. And Zeihan argues that is what the country’s decision makers have decided to do.

A demographic-economic-financial model

In his talks and writing, Zeihan describes a model of how demographics are linked to economics and finance that I’ve found quite fascinating. It is a model that stems from an acknowledgement that 1) the production of goods, services, and capital in an economy ultimately comes from the aggregate useful activity of the people, 2) people exhibit different behavior regarding consumption, production, and investment at different stages of life, and 3) those patterns of behavior are largely consistent across time and geographies. It goes something like this…

Demographers map the population of societies on a histogram with the oldest people at the top and newborns at the bottom. Throughout most of human history, these histograms looked like nice, neat triangles; there were always more young people than old people.

Industrialization completely changed this dynamic. As people began moving into cities, they started having fewer kids. The nice, neat pyramids started becoming more column-like.

The phenomenon of declining birth rates played out over several decades and we are now moving into a world were several countries — mostly developed ones — have demographic pyramids that are upside down, with more old people than young people.

Let’s call these three demographic pictures structural patterns. Every society on earth can be mapped to one of these patterns or a transition phase between them. Juxtaposed against the structural patterns are the behavior patterns. They look something like this…

Younger adults (between the ages of 25 and 45ish) form the primary consumption group. Traditionally, this group was in the process of family formation which drove a lot of consumption. They are relatively lower skilled, hence they earn less income. And their consumption needs mean they can only save a small portion of that income. Hence, they do not generate much capital for investment. But they generate the brunt of the demand that incentivizes the whole system of production to churn out stuff.

Older adults (45–65) represent the highly skilled labor. They are the most productive part of the economy and generate the highest income. Traditionally, they also consumed less per capita since the kids were on their way out by this point. Hence, they generated most of the capital for investment* in the economy.

Retirees (65+) are in the process of disconnecting from the economic system which they contributed into their whole adult lives. They do not produce and therefore do not generate income, and hence don’t generate savings for investment. They liquidate their risky investments and pour money into safer assets. Living off a fixed income, this age cohort does not add much consumption demand to the economy either. And they draw down on resources via healthcare and pension programs.

Let’s now apply this demographic-economic-financial model to the Zeihan’s historical-political narrative:

The Millennial cavalry

One thing that happened after WWII is that America set up a global system of trade protected by American military assets in order to win allies against the Soviets. This formed the underpinning of the modern global trade system as we’ve already discussed. Another thing that happened after WWII was that everyone around the world had a bunch of kids. We call these kids Baby Boomers.

As the world sought to rapidly industrialize, the Boomers provided the young energy and labor needed in the factories. And they also provided the global demand that would ultimately finance those factories. This allowed countries to grow their economies via export into a massive global consumer population.

But there is one thing that Boomers throughout most of what we call the “developed world” didn’t do — they didn’t have kids of their own. When they entered middle-age, starting in the 90s, their incomes expanded along with their savings. The Boomers became the source of a massive global capital glut allowing interest rates to fall to historic lows and sustain at those levels for decades. This capital was available for use in business investment throughout the world. Now that they had savings to play with, the Boomers were eagerly looking for a return.

This produced a “goldilocks” scenario as Zeihan describes. Starting in the 90s and extending out to the mid 2010s, global capital availability and productivity were extremely high relative to the population, consumption was still stable, and we had a secure and well developed system of global integration so the goods and capital could get to wherever they were needed easily and safely…oh, and the Cold War was over. A period of low inflation, stable economic growth, and geopolitical stability ensued. Everyone (in the “developed world”) got nice and cozy.

Baby Boomers today are between 58 and 76 years of age. Globally, they will shift into mass retirement this decade. With that, they will shift, en masse, from one economic behavior pattern to another. That is, they will shift from a high productivity, capital intensive, medium-consumption pattern to a low-productivity, low-investment, low-consumption pattern. And in most of the developed world, the upcoming generation is not big enough to replace them. According to Zeihan, this will generate massive inflationary pressure and reduce capital availability around the world.

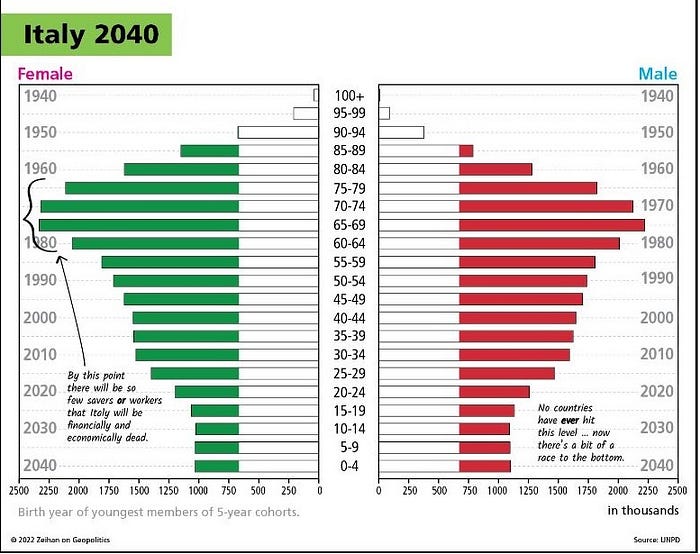

Zeihan predicts demographic-led economic collapse in major economies around the world in relatively short order. Countries like Germany and China, along with several others, have demographic profiles that are so inverted that they cannot reverse it through internal birth rates. And their largest age cohort is moving into mass retirement now, ceasing to contribute either production or capital. As the American security guarantee of global trade recedes and their largest and most productive workers leaving the workforce, the ability of these countries to even sustain current levels of exports will face headwinds, let alone grow them. And due to the demographic imbalance, during the period of American-supported global trade, many of these economies shifted to export oriented economic models to sustain their growth. For example, Zeihan believes the problem is quite acute in Europe.

Of the EU states, demographics have already turned irrecoverably past terminal in Austria, Luxembourg, Portugal, Belgium, Germany, Italy, Estonia, Latvia, Lithuania, Poland, Malta, Slovakia, the Czech Republic, Hungary, Romania, Bulgaria, Croatia, and Greece. Barring historically unprecedented baby booms, Denmark, Finland, Ireland, Sweden, the Netherlands, the United Kingdom, Spain, Greece and Cyprus are less than 15 years behind (while not EU states, Norway, the UK and Switzerland fall into this second group). Few government policies are good at bolstering birth rates, and even runaway success wouldn’t generate a new crop of consumers for a quarter-century.

Obviously, demographic collapse has its own implications for Europe’s competitiveness crisis, but it also makes the Europeans far more vulnerable to global shifts than they otherwise would be. Having a population structure which is heavy on soon-to-be retirees means Europe today is currently heavy on mature workers. Such workers are productive, but they lack European consumers to absorb their production. The EU has in effect aged into an export union, one that is utterly dependent upon exporting its excess output to the rest of the world. Germany in particular is heavily dependent upon sales to China.

So long as the Americans are holding up civilization’s ceiling and absorbing scads of output, this works. But the Americans are letting the global system collapse. For the EU this is tragic — it exports upwards of half of its manufacturing output and imports roughly 90% of its oil and natural gas needs, this imminent shift is flat-out disastrous.

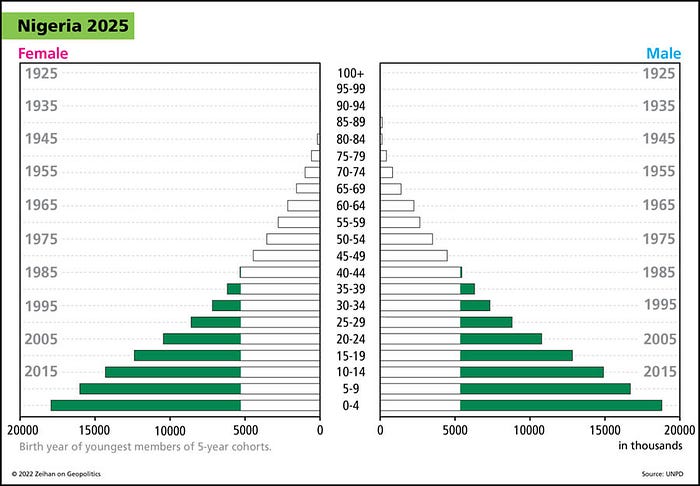

There are only two advanced economies where the Baby Boomers generated a large cohort of children — New Zealand and the United States. The Millennials in the U.S. will provide a consumption pool for the domestic U.S. economy to sell into that other developed economies won’t have, justifying investments into building up the country’s manufacturing base. For countries that the U.S. signs new trade agreements with, they may also be able to tap into that consumer base to fund their production. And as the Millennials age, they will be able to provide a base of capital for investment. While this doesn’t mean the U.S. will be able to completely ward off inflation and other shocks, the existence of a large Millennial cohort will insulate the U.S. from the sustained and dramatic economic decline Zeihan anticipates in other major economies.

In summary

What we call “globalization,” or the “global, rules-based Order,” is actually an international trade paradigm secured by the American military which was set in place post-WWII as part of a security strategy to win allies against the Soviets. Over the next seventy years, nations around the world industrialized, supported by a massive baby boom generation, and a subsequent decline in birth rates (caused by the industrialization/urbanization process). This generation provided the labor and consumption pool to drive industrialization in the early phase of the Order and the skill and investment capital in the latter phase.

More and more countries grew richer through exports by connecting into this trade system and the wealth of the world increased. However, in the early 1990s, the Soviet Union fell and the security interest underpinning America’s involvement in the Order disappeared, requiring a serious re-evaluation. For a while, America did not give this situation the attention it deserved, but by the mid-2010s, it could not be ignored any further. America’s decision makers appear to have decided on retreating from securing the global Order as they once did, knocking out the security guarantee that underwrote the system.

This will force a dis-integration of global trade and international relations. America is likely to bring manufacturing closer to home in the coming years. And, as the world moves into this new era and seeks a new type of order, America is well positioned, due to geographic, demographic, and other factors, to continue to be a major power player.

Next up?

In our discussion of T.X. Hammes’ 2016 article, we saw an analysis of how modern technological changes will alter the business logic of production, pushing manufacturing closer to its end markets. From our discussion of Peter Zeihan’s views we understand how a changing security and demographic landscape has shifted America’s strategic interests away from securing global trade at a time when rapidly aging populations will make economic growth harder to achieve all over the world.

The next analyst we will look at arrived at his prediction of de-globalization by studying a very interesting and counterintuitive macroeconomic phenomenon. One that he believes will shift the most valuable economic activity from globalization to localization. Without giving away too much, I’ll just say this: it is common to worry about the risks of failure, but it’s important to remember that success also brings its own set of risks.

*Intuitively, this model of aggregate capital generation makes sense to me. But after having lived through over a decade of quantitative easing by the largest economies in the world, where central banks were directly involved in monetizing financial assets, I wonder if Zeihan’s model is sufficient to explain a (powerful) nation’s ability to generate capital. Is America, the issuer of the global reserve currency, really dependent on the savings of its people to finance investment? Admittedly, there is still a lot I need to learn to understand the mechanism(s) connecting domestic savings to the total money supply. I do hope, though, that Zeihan’s model is correct, because it would make the financial system feel like it makes sense, that it is somehow “correct” and “balanced” and “tethered to reality,” rather than arbitrary and “disconnected from reality.” The recent rise in interest rates and persistent inflation do support Zeihan’s model.

Zeihan is currently in the middle of a series explaining the fundamentals of the global demographic picture in his newsletter. Highly recommend you check it out if you are interested in digging more into the demographic-economic-financial model described above.

For other references and disclaimers check out the links in the articles or scroll to the bottom of Part 1.

Hope you enjoyed this article. If you have any comments or critiques, please share!